Mr. Tan

You explained that a life insurance policy using a yield of 4.75% actually work out to 2% after removing the "effect of deduction". Surely, a 2% yield is satisfactory compared to 1% (or less) paid by bank deposit? The policyholder also get life insurance protection.

REPLY

If you are investing for 10 or 15 years, a yield of 2% is not satisfactory. You should aim for a yield of 5%. The difference between a yield of 2% and 5% can be a large sum. Here is a way for you to find out.

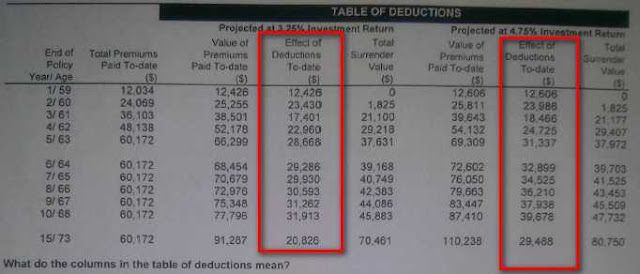

In the benefit illustration, you can see a page called "Table of Deduction". It shows you the "Value of Premiums Paid to Date", "Effect of Deduction" and "Total Surrender Value".

See the example below.

On the maturity date (i.e. end of 15 years), the value of premiums paid to date is $110,238, the effect of deduction is $29,488 and the total surrender value is $80,750. The total premiums paid is $60,000. The insurance company took your premium and invest them to earn 4.75%, and at the end of 15 years, they take away $29,488 and leave you a net return of $20,750.

If you invest the money on your own, you will get $50,238 on top of the $60,000. Why give away $29,488 to the insurance company when they do not provide any tangible benefit?

IF you invest on your own in the STI ETF, you should be able to get a return of 5% or more, and the risk is not different from the risk that is inherent in the insurance policy, i.e. the surrender value is not guaranteed and is subject to the insurance company earning 4.75% yield.

If you terminate the policy before maturity, you suffer a bigger effect of deduction. Look at the figures for year 5 to 15. You could be losing 50% of your premium.

For this policy, there is virtually no life insurance protection. The death benefit is only 5% more than the total premium paid.

You explained that a life insurance policy using a yield of 4.75% actually work out to 2% after removing the "effect of deduction". Surely, a 2% yield is satisfactory compared to 1% (or less) paid by bank deposit? The policyholder also get life insurance protection.

REPLY

If you are investing for 10 or 15 years, a yield of 2% is not satisfactory. You should aim for a yield of 5%. The difference between a yield of 2% and 5% can be a large sum. Here is a way for you to find out.

In the benefit illustration, you can see a page called "Table of Deduction". It shows you the "Value of Premiums Paid to Date", "Effect of Deduction" and "Total Surrender Value".

See the example below.

On the maturity date (i.e. end of 15 years), the value of premiums paid to date is $110,238, the effect of deduction is $29,488 and the total surrender value is $80,750. The total premiums paid is $60,000. The insurance company took your premium and invest them to earn 4.75%, and at the end of 15 years, they take away $29,488 and leave you a net return of $20,750.

If you invest the money on your own, you will get $50,238 on top of the $60,000. Why give away $29,488 to the insurance company when they do not provide any tangible benefit?

IF you invest on your own in the STI ETF, you should be able to get a return of 5% or more, and the risk is not different from the risk that is inherent in the insurance policy, i.e. the surrender value is not guaranteed and is subject to the insurance company earning 4.75% yield.

If you terminate the policy before maturity, you suffer a bigger effect of deduction. Look at the figures for year 5 to 15. You could be losing 50% of your premium.

For this policy, there is virtually no life insurance protection. The death benefit is only 5% more than the total premium paid.

No comments:

Post a Comment